A waiver of subrogation is a common clause in construction contracts that defines how risk and responsibility are shared after an accident or loss. It prevents one party’s insurer from suing another involved party, helping teams focus on completing the project instead of settling blame.

This guide covers how a waiver of subrogation works, when to use it, and what to check before signing. Understanding it helps you manage risk and avoid costly disputes.

Waiver of Subrogation Meaning

A waiver of subrogation is a legal agreement in a contract or insurance policy that gives up the insurer’s right to recover money from another party responsible for a loss. In short, once your insurer pays your claim, they cannot go after the person or company that caused the damage.

There are two main types of waivers of subrogation:

- Specific waiver: applies to one contract or project only. It’s issued for a single situation and must be listed in the policy or contract.

- Blanket waiver: applies automatically to all contracts or agreements that require it. It offers broader protection but usually costs more.

A waiver of subrogation clause appears in contracts to prevent lawsuits between business partners, landlords, tenants, or contractors. It keeps projects and relationships running smoothly without disputes over fault. However, it also limits your insurer’s options and may affect coverage or premiums if not approved in advance.

Why Waiver of Subrogation Matters in Contracts and Insurance

A waiver of subrogation is important because it affects how financial responsibility and insurance claims are handled after a loss. It helps businesses prevent conflicts and protect their insurance relationships.

Here are the main reasons it matters:

- It stops one party’s insurer from suing another party involved in the same project.

- It reduces legal disputes and keeps business operations running smoothly.

- It helps maintain trust between contractors, clients, and partners.

- It can influence insurance coverage, claim handling, and premium costs.

- It’s often required in contracts to limit liability and streamline claims.

For example, if a contractor damages a client’s property, the client’s insurer covers the loss. With a waiver of subrogation, the insurer can’t sue the contractor for repayment, preventing unnecessary legal battles and keeping the business relationship intact.

Where You’ll Commonly See a Waiver of Subrogation

You’ll often find a waiver of subrogation in contracts where multiple parties share financial or property risks. These agreements include the clause to prevent one side’s insurer from pursuing the other after a loss.

Here are the most common places you’ll encounter it:

You’ll most often see a waiver of subrogation in industries where contracts involve shared risk, like construction, leasing, and professional services. It’s common in any agreement that needs to protect business relationships and avoid insurance disputes between parties.

How Does a Waiver of Subrogation Work in Construction Contracts?

In construction, a waiver of subrogation prevents insurance companies from suing other project participants after paying a claim. It keeps projects on track and avoids blame disputes between contractors, owners, and subcontractors.

Here’s how it works in practice:

- The contract requires all parties to include a waiver of subrogation in their insurance policies.

- Each insurer agrees not to recover money from any other party involved in the project.

- If damage occurs, the insurer pays the claim and waives its right to sue others for reimbursement.

- The clause applies only after payment and must be endorsed by the insurer to be valid.

Here’s an example to make it clear:

Imagine a subcontractor accidentally damages an on-site structure. The general contractor’s insurance pays for the repairs. Thanks to the waiver of subrogation in the contract, the insurance company cannot sue the subcontractor to recover the money.

What’s the result? The issue is resolved, relationships are preserved, and everyone gets back to work. This clause is an important aspect of contract administration, where managing risks and resolving claims efficiently is critical.

Here’s what you should know about a waiver of subrogation:

- It’s typically included in general liability, workers’ compensation, or property insurance policies.

- Insurance providers often charge higher premiums for policies that include the waiver.

- The waiver only applies to claims that fall under the scope of the specific policy.

Why Should You Include a Waiver of Subrogation in Construction Contracts?

Aside from waiver of subrogation being a legal formality, it’s a practical tool to keep construction projects on track. By preventing lawsuits between project stakeholders, this clause encourages collaboration and reduces conflict.

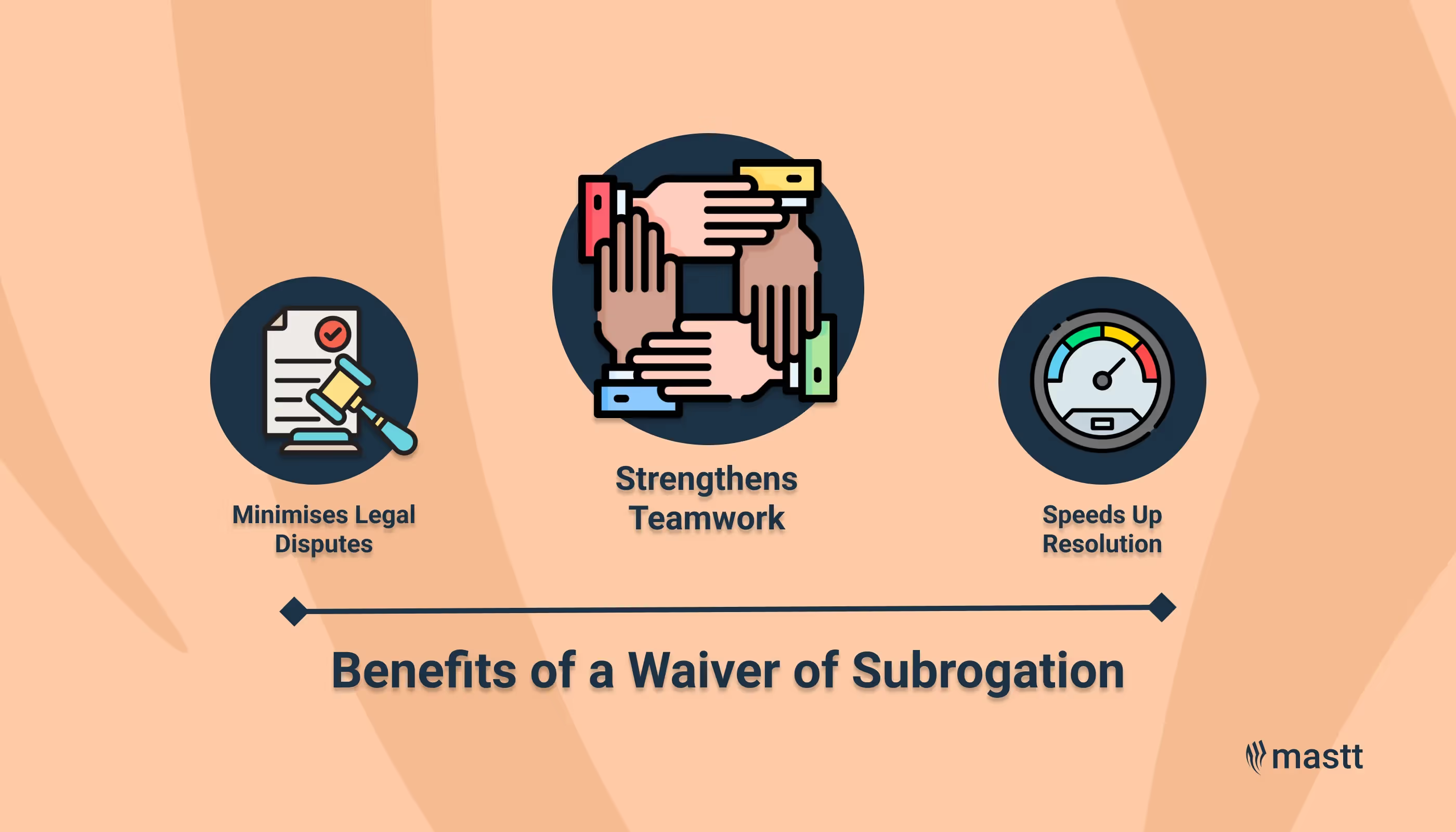

Here are the benefits of a waiver of subrogation:

- Minimises Legal Disputes: Insurance companies can’t involve others in lawsuits over covered claims.

- Strengthens Teamwork: Stakeholders can focus on the project without fear of legal backlash.

- Speeds Up Resolution: Claims are settled faster since disputes are avoided.

For example, if a subcontractor’s mistake damages expensive equipment, the general contractor’s insurance handles the claim. The waiver of subrogation stops the insurer from suing the subcontractor.

This approach is particularly useful when combined with milestones like the certificate of practical completion, which signals the project is ready for handover and reduces further risks.

This saves time, avoids delays, and ensures everyone keeps working together. Isn’t that what every construction team wants—a smooth, conflict-free process?

What to Check Before You Sign a Waiver of Subrogation

Before you agree to a waiver of subrogation, review how it changes your coverage, premiums, and risk. Every detail matters because once signed, you give up your insurer’s right to recover costs from others.

Here’s what to check carefully:

- Policy Approval: Confirm your insurer allows waivers under your policy. Some carriers require written consent or a special endorsement before it becomes valid.

- Type of Waiver: Identify whether it’s a blanket waiver or a specific one. Blanket waivers give broad protection but can increase costs.

- Premium Impact: Ask your insurance provider if the waiver could raise your premium. Many insurers charge extra since they lose recovery rights.

- Coverage Scope: Make sure the waiver only applies to covered claims under your policy. It shouldn’t affect unrelated incidents or other policies.

- Contract Consistency: Ensure every party in the agreement uses the same waiver terms. Inconsistent wording can create gaps in coverage and disputes later.

- Endorsements: Check that all required endorsements are attached to your insurance policy before signing. Without them, the waiver may not hold up if a claim occurs.

A waiver of subrogation protects relationships but can change who carries the financial risk. Always review the clause with your insurance agent or legal advisor to ensure you’re not giving up more than intended.

Pros and Cons of a Waiver of Subrogation

The main advantage of a waiver of subrogation is that it prevents lawsuits and keeps business relationships intact. The main drawback is that it can raise insurance costs and shift more risk to you. Still, not all situations benefit from having this clause.

Here’s a quick look at both sides:

💡 Pro Tip: Always send waiver of subrogation requirements to your insurance broker before binding coverage - not after. This prevents premium surprises and ensures your policy actually includes the endorsement you need.

How Much Does a Waiver of Subrogation Cost?

A waiver of subrogation typically costs between $50 and $500, depending on your policy type, contract size, and industry risk. Some insurers charge a flat fee per waiver, while others add 2% to 5% to your total premium if it’s a blanket waiver covering multiple contracts.

Here’s what usually affects the price:

- Type of Insurance: General liability and workers’ compensation waivers tend to be on the lower end, while property insurance waivers cost more.

- Scope of the Waiver: Blanket waivers are more expensive because they apply to all contracts, not just one.

- Industry Risk Level: Construction, real estate, and manufacturing businesses often pay the highest rates due to higher claim exposure.

- Policy Terms: Older or high-limit policies may have higher fees since they carry more potential loss.

The key is balancing cost with contract requirements. If waivers are common in your line of work, negotiating a blanket waiver can be more cost-effective than paying for multiple single-use ones.

When Should You Use a Waiver of Subrogation?

You should use a waiver of subrogation when maintaining collaboration and avoiding legal disputes matter more than assigning fault. It’s especially valuable in projects or agreements where several parties share risks, such as construction, leasing, or service contracts.

Here are situations where adding a waiver makes sense:

- Construction Projects: Prevents contractors, subcontractors, and owners from suing each other’s insurers after a loss.

- Large-Scale Projects: Reduces the chance of disputes when multiple teams work together and one incident could delay progress.

- High-Risk Jobs: Useful for industrial, infrastructure, or manufacturing projects where accidents are more likely.

- Lease and Service Agreements: Keeps landlords, tenants, and vendors from turning claims into lawsuits.

- Contractual Requirements: Often mandatory when project owners or clients include it as part of their risk management terms.

- Joint Ventures or Partnerships: Promotes cooperation when both parties rely on shared assets or property.

Use the waiver when the goal is to keep operations running smoothly and reduce the chances of lawsuits. However, always confirm that your insurer allows it and understand how it might affect your coverage or premiums before adding it to any agreement.

This clause works hand-in-hand with avoiding risks like termination of contract, which could disrupt the project entirely.

Does a Waiver of Subrogation Fit Your Construction Needs?

A waiver of subrogation can reduce disputes and keep construction projects running smoothly, but it also shifts some risk to the policyholder. Contractors, subcontractors, and project owners should weigh the costs, coverage limits, and project conditions before agreeing to it.

If your work involves high-risk or multi-party projects, adding this clause can protect relationships and prevent costly delays. Always confirm the details with your insurer or legal advisor to ensure you stay fully covered.

Written by

Jefbeck Eje

Jefbeck is an SEO Specialist at Mastt who creates optimized content for the construction project management industry. Focused on delivering accurate and actionable insights, Jef combines SEO expertise with industry knowledge to enhance visibility, build authority, and drive engagement. His work ensures Mastt remains a trusted resource for construction professionals seeking reliable information.

Contributions by

Contract Review Checklist

Use this contract review checklist to review construction agreements with clarity. Track contract terms, obligations, risks, and compliance in one structured document before signing.

Walk Into Every Meeting With Confidence, Clarity, and Control

No one wants to look unprepared, blindsided, or uncertain in front of stakeholders — but that’s exactly what happens without Mastt.

Start for FreeTrusted by the bold, the brave, and the brilliant across governments, Fortune 500s, and the world’s best in delivering the future

.avif)

.avif)