Construction invoice factoring gives contractors a way to turn slow-paying invoices into fast working capital. Instead of waiting weeks or months for a general contractor or owner to release payment, you sell the invoice to a factoring company and get most of the cash upfront.

In this guide, you’ll learn what construction invoice factoring is, how it works, what it costs, and how it compares with other financing options. You’ll also see who qualifies, what documents you’ll need, and how to pick a factoring partner.

What is Construction Invoice Factoring?

Invoice factoring in construction is the process of selling your unpaid invoices to a factoring company in exchange for a cash advance. Instead of waiting for long payment terms, you get most of the invoice amount upfront, usually within a day or two. It gives contractors fast access to working capital tied up in construction invoicing.

Invoice factoring is not a loan. You aren’t adding debt or taking on interest. You’re simply converting an outstanding invoice into usable cash while the factor waits for the general contractor or owner to pay. Many contractors use it when they need funds for payroll, materials, equipment, or to keep work moving during long draw cycles.

Common Types of Construction Invoice Factoring

Contractors have several types of construction invoice factoring to choose from, including recourse and spot factoring. Each one works differently based on risk, flexibility, and cash flow needs.

Here are the most common types of invoice factoring contractors rely on:

Most contractors choose recourse factoring because it offers low fees and high advance rates. Non-recourse and contract-based options work well in specific situations but usually cost more. The goal is to match the factoring type to your billing style, your customer’s payment habits, and the cash flow needs of your projects.

Why Contractors Use Invoice Factoring

Contractors use invoice factoring to keep work moving when payment terms exceed their cash reserves. It turns slow-paying invoices into working capital they can use right away. This helps stabilize construction invoicing cycles that often run 30, 60, or even 90 days.

- Steady Cash Flow: Factoring gives you fast access to cash so you can cover project costs without waiting on a general contractor or project owner to pay.

- Predictable Payroll: You can pay crews on time, even when approved pay apps get held up in the review process.

- Pay Suppliers Without Delays: Early cash helps you stay current with material yards, rental companies, and specialty suppliers.

- Flexible Approval for Lower Credit Scores: Factors look at your customer’s credit, not yours, which helps newer or smaller contractors get funded.

- Reduced Debt Load: You’re not adding loans or interest-heavy balances to your books.

- Unlock Growth Capital: You can take on more work or start new jobs without cash flow slowing you down.

- Avoid High-Cost MCA Loans: Factoring replaces daily withdrawals and heavy interest with a simpler fee tied to the invoice.

Many contractors turn to factoring after dealing with retention, slow inspections, and long approval cycles that strain their working capital. Having predictable cash lets them keep crews productive, buy materials sooner, and avoid project slowdowns.

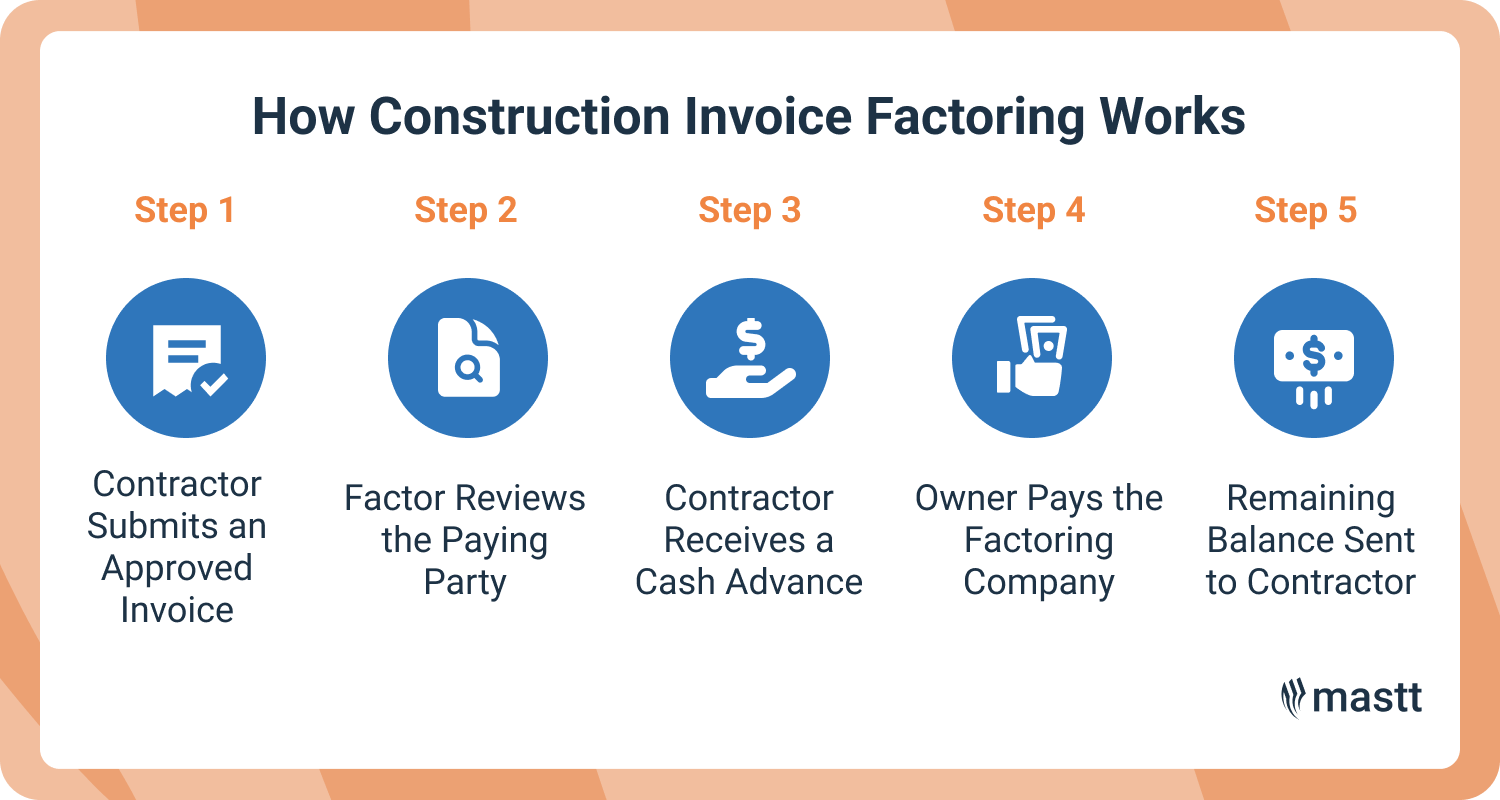

How Construction Invoice Factoring Works

Construction invoice factoring starts when you submit an approved invoice or pay application to a factoring company. They review the paying party, advance most of the invoice value, collect payment from the GC or owner, and then send you the remaining balance. It follows the same flow as construction invoicing, only with the cash landing much earlier in the cycle.

1. Contractor Submits an Approved Invoice or Pay App

First, you complete the work for the billing period and submit your pay application or invoice to the GC or owner as normal. Once they approve it, you send that same approved invoice package to the factoring company.

The “invoice package” usually includes the invoice or pay app, backup like timesheets or delivery tickets, and any required sign-offs. Most factors use an online portal where you upload documents, tag the customer, and confirm the billed amount. The clearer your documentation, the faster they can review and fund it.

2. Factoring Company Reviews the Paying Party

Next, the factoring company looks at the credit strength and payment history of the GC or owner who owes the money. They care more about whether your customer pays on time than about your own credit score.

They may run a credit check, review trade references, and look at how long your customer usually takes to pay invoices. If the account looks solid and the terms are clear, they approve the invoice. They also set a credit limit for that customer to control their risk exposure.

3. Contractor Receives an Upfront Cash Advance

Once the invoice is approved, the factor advances a percentage of the invoice value to your business bank account. In construction, this advance is often in the 70-90% range, depending on risk and terms.

Funding usually lands within 24 to 48 hours after approval, sometimes faster once you’re an existing client. You can use that cash for payroll, suppliers, rentals, or any cost tied to active jobs. The remaining portion of the invoice becomes a reserve that the factor holds until the customer pays in full.

4. GC or Owner Pays the Factoring Company

After funding, the factor notifies the GC or owner that they should pay the factoring company instead of your business. This is normally done through a “notice of assignment” that explains where to send payment and how to reference your account.

From that point on, payments on those factored invoices go directly to the factor. They track due dates, follow up on slow payments, and reconcile what has been collected against each invoice. This also reduces the time your team spends chasing checks and matching remittances.

5. Remaining Balance Sent to Contractor

When the GC or owner pays the invoice in full, the factoring company deducts its fee and releases the remaining reserve balance to you. For example, if they advanced 85% upfront, they send you most of the remaining 15% after subtracting the agreed factoring fee.

You’ll see this final settlement on a statement that breaks down the invoice amount, fee, and net amount wired to your account. Over time, you can track how long each customer takes to pay and how that impacts your total cost of factoring.

Many contractors run only select customers or projects through factoring at first, then expand once they see how the cash flow lines up with their schedule of values.

Invoice Factoring vs Other Construction Financing Options

Construction invoice factoring differs from other financing tools because it converts unpaid invoices into working capital without adding debt. Other options rely on credit scores, collateral, or repayment schedules that don’t always align with long construction payment cycles.

Here’s a quick overview of how it compares to other common construction financing options:

Invoice factoring often fits construction better because it follows the flow of pay applications, approvals, and typical payment delays. When comparing options, line up each one with a real project timeline. Any product that pulls cash from your account before the GC pays the invoice can create more pressure than it solves.

What Construction Factoring Costs: Rates and Fees

The factoring rate depends on the invoice amount, how fast the GC or owner pays, and the risk tied to the construction project. Most factors charge a simple fee based on how long the invoice remains outstanding. You get most of the invoice value upfront, and the fee comes out when the owner pays.

Here are the most common charges contractors see:

- Initial Fee: This covers the first billing period, often the first 30 days, and usually ranges from about 1% to 3% of the invoice value.

- Incremental Fees: These apply if the GC or owner takes longer than the initial period to pay, and they’re charged in smaller steps, usually around 0.25% to 1% per extra period.

- Wire or ACH Fees: Some factoring companies charge a small fee for sending funds to your bank account, depending on the transfer method you choose.

- Setup or Due Diligence Fee: A few factoring companies add a one-time fee to set up your account, review documents, or pull customer credit.

- Reserve Release: This isn’t a fee, but it’s part of your cost. The factor holds a percentage of the invoice (often 10% to 20%) and releases it after the GC or owner pays, minus the factoring fees.

Payment speed has the biggest impact on your total cost. Faster-paying customers lower your incremental fees, while slow-paying customers increase the overall cost because the invoice stays open longer. Contractors who factor regularly often negotiate better pricing or volume-based discounts.

Who Qualifies for Construction Invoice Factoring?

Most contractors and subcontractors can qualify for construction invoice factoring as long as they bill creditworthy customers and have approved invoices or pay applications. The factoring company focuses more on the GC or owner’s payment history than on your personal credit score.

- Subcontractors Billing on 30-90 Day Terms: Trades like electrical, plumbing, HVAC, concrete, and framing often qualify because they bill predictable scopes of work.

- General Contractors with Slow-Paying Owners: GCs who manage multiple pay apps across long schedules benefit from factoring when owner payments lag.

- Contractors Working with Creditworthy GCs or Owners: Firms with customers who pay reliably are strong candidates because factoring companies evaluate the paying party’s credit strength.

- Construction Businesses That Need Steady Working Capital: Construction companies taking on larger jobs or more frequent draws qualify because they generate consistent monthly billings.

- Small or New Contractors with Weak Credit: Factors often approve newer businesses, since customer credit matters more than the contractor’s personal score.

- Construction Companies with Multiple Projects at Once: Contractors juggling several active sites qualify because their billing volume produces repeatable, fundable invoices.

Most factoring companies also look for basic documentation, like your customer list and approved invoices, but the main qualifier is who you work for and how reliably they pay. Strong-paying GCs and owners lead to faster approval, higher advance rates, and smoother funding.

What are the Documents Needed to Apply for Invoice Factoring?

You only need the same documents you already use for invoicing, project billing, and compliance to apply for construction invoice factoring. These documents help the factor confirm your business details, the work completed, and the customer’s ability to pay.

☑️ Business Information: Basic details like your license, EIN, and company background confirm you are a registered contractor.

☑️ Project Contracts: Signed agreements, approved change orders, and clear payment terms help the factor verify the scope and billing structure.

☑️ Invoice Package: Your pay app, progress report, timesheets, material receipts, and other backup show the work was completed and approved.

☑️ Compliance Items: Certificates of insurance, lien waivers, and safety documentation ensure that the project meets legal and contractual requirements.

☑️ Customer Details: The GC or owner’s credit profile, payment history, and contact information allow the factor to evaluate risk and set credit limits.

💡 Pro Tip: Create a standard “factoring packet” for every project with contracts, approved pay apps, and compliance items in one folder. Contractors who do this often cut their funding time from days to hours because their paperwork is already organized and ready to upload.

What Happens After You Apply for Construction Invoice Factoring

After you submit your documents, the factoring company reviews your customers, sets up your account, and prepares your funding schedule. The process moves quickly because approval depends on the GC or owner’s payment record, not your credit score.

- Credit Review of Your Customers: The factor checks the GC or owner’s payment history to confirm they reliably pay invoices.

- Setting Customer Credit Limits: The factor assigns a credit limit to each GC or owner so they know how much they can safely advance.

- Account Setup and Agreement: You receive a factoring agreement that outlines fees, advance rates, and how funding will work.

- UCC Filing on Receivables: The factor files a UCC (Uniform Commercial Code) notice so they can legally secure the invoices they fund.

- Portal Access and Invoice Submission: You get login details for the online portal where you’ll upload pay apps or invoices for funding.

- First Funding Release: Once your first approved invoice is submitted, the factor advances the agreed percentage to your bank account.

Most contractors receive their first funding within a few days, and repeat funding moves faster after the factor has reviewed your customers and set credit limits. As relationships grow, many factors reduce paperwork or speed up approvals for future invoices.

Invoice Factoring Risks and How to Handle Them

The main risks in construction invoice factoring involve repayment responsibility, contract restrictions, and how the factor interacts with your customers. Contractors should understand these risks clearly before committing to an agreement:

💡 Pro Tip: One way to reduce factoring risks is to make sure your billing documents are accurate before they reach the factor. Mastt’s AI Payment Review helps by scanning pay apps and invoice packages for errors, missing backup, or inconsistencies that could lead to disputes.

How to Choose a Reliable Construction Invoice Factoring Service

You can determine a trustworthy construction factoring company by checking their experience in billing and how they handle communication with your GCs or owners. The goal is to work with a partner who understands your projects and supports your cash flow without creating new problems.

- Look for Construction Experience: Choose an invoice factoring company that works with contractors and understands pay apps, retention, and progress billing.

- Check Their Advance Rates and Fees: Make sure the rates match the type of work you perform and the payment speed of your customers.

- Review Their Collection Process: Confirm they contact your GCs or owners professionally and keep communication clear.

- Ask About Factor Funding Speed: A strong factoring partner funds consistently within 24 to 48 hours once your invoices are approved.

- Confirm Portal and Support Tools: A good portal makes it easy to upload pay apps, track invoices, and check payment status.

- Assess Contract Terms: Look closely at minimum volume requirements, termination fees, and how recourse works.

- Check Their Customer Credit Review: Strong underwriting protects you from funding invoices tied to risky customers.

💡 Pro Tip: Ask the factor to walk through a real pay app from one of your current jobs. If they can explain how they’d fund it and what documents they need without hesitation, they understand construction well enough to support your cash flow.

When Construction Invoice Factoring is the Right Move

Construction invoice factoring makes sense when long payment cycles slow down the work you already have lined up. If your cash is tied up in approved pay apps or you’re juggling payroll, factoring can stabilize your cash flow without taking on new debt. It gives contractors a way to keep projects moving, cover costs on time, and take on new work with confidence.

Written by

Anna Marie Goco

Anna is a seasoned Senior Content Writer at Mastt, specialising in project management and the construction industry. She leverages her in-depth knowledge to create valuable content that helps professionals in these fields. Through her writing, she contributes to the company's mission of empowering project managers and construction professionals with practical insights and solutions.

Contributions by

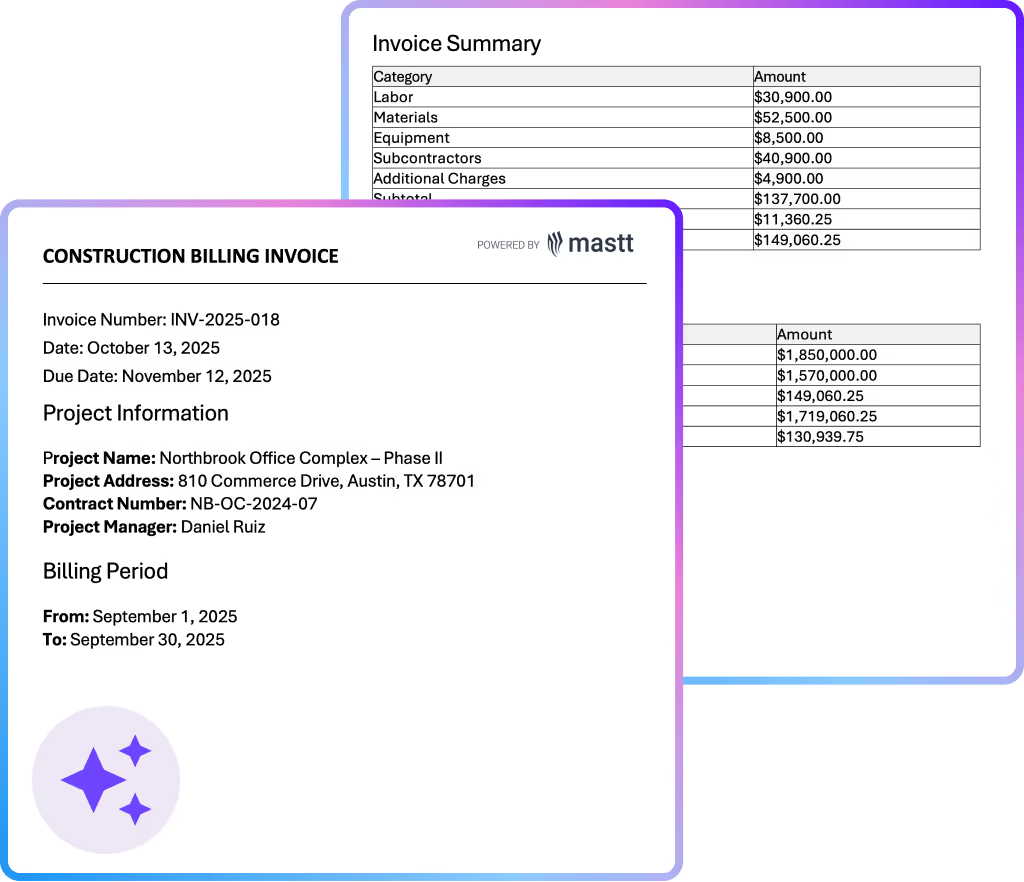

Construction Billing Invoice Template

Use this construction billing invoice template to manage progress payments, track billing cycles, and document work completed. Keep billing consistent across all construction projects with standardized formats.

Walk Into Every Meeting With Confidence, Clarity, and Control

No one wants to look unprepared, blindsided, or uncertain in front of stakeholders — but that’s exactly what happens without Mastt.

Start for FreeTrusted by the bold, the brave, and the brilliant across governments, Fortune 500s, and the world’s best in delivering the future

.avif)