Post author:

Stephanie Flores

Construction budgeting is the disciplined process of planning, forecasting, and controlling project costs across the lifecycle. Learn how to build a detailed construction budget, manage risk, and prevent overruns with effective cost control.

Use this FREE Construction Budget Template to estimate and manage project costs with confidence. Track direct and indirect expenses, monitor actual vs planned spend, and maintain clear financial oversight.

Construction budgeting is the financial framework used to plan, allocate, and control costs throughout a project. It defines the expected total cost, organizes expenses into clear budget categories, and sets the structure for tracking spending as work progresses.

This guide explains how construction budgeting works in practice and how teams manage costs throughout the project lifecycle. It also outlines the best practices and common mistakes that shape effective budget management in real projects.

Construction budgeting is the structured process of planning, approving, and managing all costs required to deliver a construction project. It converts defined scope into an authorized financial plan that governs spending during execution.

The construction project budget sets the approved cost baseline and defines how expenses will be recorded, reviewed, and updated. It organizes direct costs, indirect costs, overhead, and contingency into traceable budget categories aligned with scope and contract commitments.

It also establishes how financial performance is measured. Project teams reconcile commitments and actual costs against approved figures and update forecasts as conditions shift. A well-managed construction budget keeps cost control aligned with funding and contractual obligations.

Construction budgeting sets financial boundaries and defines how cost performance will be monitored during delivery. Without structure, even well-funded projects can lose financial control.

Construction budgeting is important because it:

Construction cost planning defines what a project should cost while the design is still evolving. Construction budgeting defines what the project is allowed to spend once scope, pricing, and funding are approved. The difference is authority: cost planning informs decisions, while budgeting controls spending.

The table below outlines how they differ in purpose, timing, and leadership.

For example, an owner’s cost consultant develops a $42M-$48M target during design. That range shifts as drawings and quantities change.

Once contracts are signed at $44.6M, the owner approves a $45M construction budget. From that point, spending is controlled against the approved limit.

An ideal construction budget should capture every cost required to deliver the approved project scope. Clear classification improves financial visibility and reduces the risk of hidden cost overruns.

A detailed construction budget typically includes the following categories:

A detailed construction budget must organize these categories under consistent cost codes and align them with the approved project scope. When cost categories reflect how the project is procured and delivered, reporting becomes clearer, and forecast updates remain dependable.

You need enough money to cover the full project cost. That includes build cost, professional fees, approvals, site works, and risk. Use this simple formula: Total Construction Budget = Hard Costs + Soft Costs + Risk Allowances + Owner Costs.

For many building projects, hard costs sit around 70% to 85%. Soft costs often land between 8% and 15%. Owner costs usually run 1% to 5%. Then add risk allowances, which commonly sit between 5% and 20%.

Use these budget buckets to total the full amount.

This table shows practical percentages you can apply today.

💡 Pro Tip: Pick numbers from the table based on design maturity and risk. Lock them into your project cost plan, then track changes through approvals and procurement. That keeps your construction budget realistic from day one.

Construction budgeting follows five stages: planning, estimating, baseline approval, forecasting, and closeout. You set scope and funding first, then track performance against the approved cost baseline through to final reconciliation.

Here are the major phases and how the budget evolves in each one:

The process starts by defining what the project includes and excludes. Teams break the project into a work breakdown structure and assign cost codes that will carry through reporting. Early risk identification improves pricing accuracy before procurement starts.

Teams translate quantities and pricing into a structured construction budget. Direct costs, indirect costs, overhead, and contingency are organized into defined categories. Contract type influences how risk is priced and how tightly cost must be monitored during execution.

After validation and approval, the project budget becomes the authorized financial reference. Teams document assumptions, formalize approvals, and define variance thresholds that trigger escalation. Locking the baseline prevents uncontrolled adjustments that weaken financial governance.

During execution, live data replaces early assumptions. Project managers track commitments, record actual costs, and update forecasts on a set cadence. Continuous reconciliation keeps projected final cost tied to contract values and site performance.

Financial management continues after construction work is complete. Teams settle final accounts, reconcile change orders, and analyze performance against the original budget. Documented cost data supports more accurate pricing on future projects.

Construction budgeting methods include traditional estimating, bottom-up, top-down, activity-based, and zero-based approaches. The right method depends on scope certainty, available data, and funding limits.

The table below outlines the most common methods and when they are most effective.

Each method influences how accurately teams control project cost. The method selected should match project complexity, risk exposure, and available cost data.

Experienced teams often combine approaches for early planning with detailed bottom-up pricing before finalizing a construction budget.

The project owner holds primary responsibility for budgeting, since funding authority and final approvals sit at that level. The project manager manages day-to-day budget control during execution. Other roles contribute technical, contractual, and financial input throughout the project lifecycle.

Clear approval pathways are essential in construction budget management. Defined authority for releasing contingency, approving change orders, and adjusting forecasts prevents confusion and delays. Financial decisions move better when accountability is visible and documented.

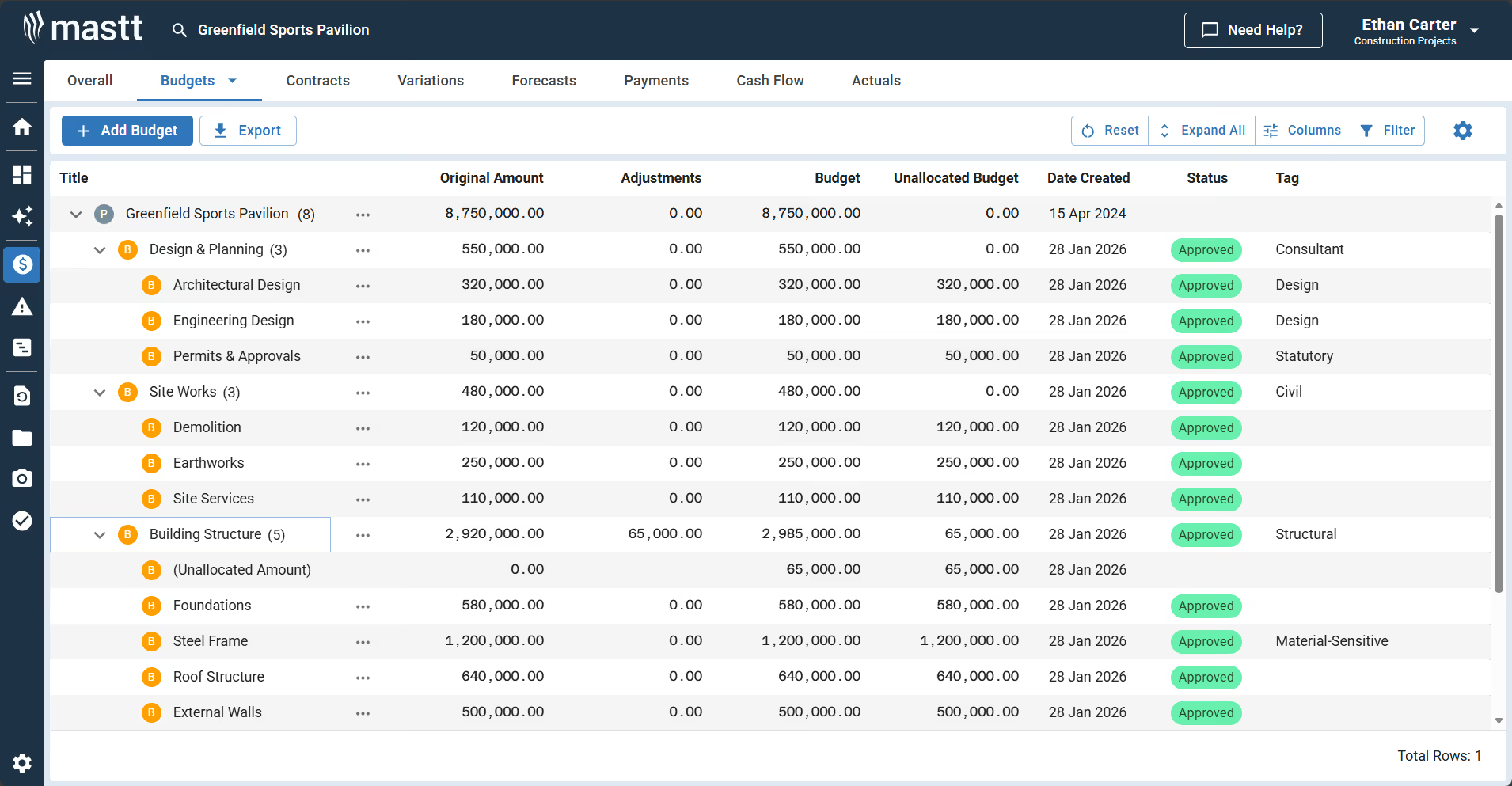

This example shows a good construction budget for the Greenfield Sports Pavilion, totaling $8,750,000. It is organized by clear cost codes and major scope categories, making financial data easy to follow. Original amounts, approved adjustments, revised totals, and remaining balances are visible in one place. It reflects what strong budget control should look like in practice.

Budgets are grouped into categories such as Design & Planning, Site Works, and Building Structure. It tracks changes clearly, including a $65,000 approved increase within Building Structure. Revised totals and remaining balances stay visible, which supports transparent oversight. This layout helps simplify cost tracking and forecasting.

Budgets fail when discipline breaks down. Most overruns stem from avoidable control gaps rather than unpredictable events. Identifying common mistakes early protects margin and funding stability.

Here are common budgeting pitfalls and practical ways to prevent them:

Most budget overruns do not happen overnight. They build gradually through small control gaps and delayed financial decisions. When teams enforce clear approval thresholds and act on early variance signals, cost exposure stays contained.

Effective budgeting in construction projects rely on structured processes and consistent oversight. Clear controls reduce ambiguity throughout the project lifecycle.

Use these best practices to keep your construction budget accurate and controlled:

☑️ Lock cost codes before procurement: Finalize the cost structure in pre-construction and avoid mid-project changes. Stable coding protects reporting and forecast integrity.

☑️ Separate contingency categories: Track owner contingency, contractor contingency, and management reserve independently. Approve drawdowns against defined risks only.

☑️ Forecast using live commitments: Base Estimate at Completion (EAC) on signed contracts and approved changes. Do not rely only on percent-complete assumptions

☑️Enforce strict change control: Require defined scope, priced impact, and funding approval before execution. Update the budget and forecast immediately

☑️Align cash flow with commitments: Check funding timing against upcoming trade awards and projected spend. Liquidity gaps create budget risk.

☑️Capture final cost data properly: Close projects with clean cost codes and documented variances. Reusable data improves future budgeting accuracy.

💡Pro Tip: Build your forecast from committed costs first, then layer in projected exposure. Centralized construction project cost management software that tracks commitments in real time produces more reliable EAC results and strengthens financial control.

Construction budgeting relies on defined tools to plan, track, and control project costs accurately. These platforms support different estimating methods, budget development, cost tracking, forecasting, and reporting. The right setup improves visibility and reduces manual errors.

To move from estimate to live cost control, most teams use these tools.

Construction budgeting is the control system that protects a project’s financial outcome. It translates approved scope and executed contracts into a controlled cost baseline, then ties that baseline to live commitments and forecast logic.

When managed properly, it exposes risk early, enforces accountability, and keeps funding aligned with delivery. Projects that treat budgeting as an active control process (not a static spreadsheet) achieve stronger financial certainty from planning through closeout.

Written by

Stephanie Flores was a Construction Content Writer at Mastt, producing long-form guides and research articles on cost management, contract management, and risk. She holds a Bachelor of Arts in Political Economy from the University of Asia and the Pacific, and completed TAFE NSW courses in construction fundamentals.

Contributions from

Cut the stress of showing up unprepared

Start for FreeTrusted by the bold, the brave, and the brilliant to deliver the future

.avif)